As the cattle market reopened following Labor Day, feeder and live cattle futures weakened to contract low levels of resistance. The October feeder cattle contract ended on a down note at approximately $230, as the market continues to grapple with whether prices will rise this fall amid uncertainty over how many heifers will go through sale barns. A significant factor contributing to current market conditions is the deterioration of pasture conditions, which has led to expectations that some feeder cattle will be brought to market earlier. However, this impact is tempered by a large hay crop and the availability of cheap feed, both of which are already being priced into the market.

Of the 12 states that contribute to the CME Feeder Cattle Index, 10 reported price declines over the past week. Nebraska, however, stood out as an exception, with a strong rebound in the prices of 500-600 lb. cattle, surging to nearly $340 per cwt. after several weeks of decline. Meanwhile, prices for 700-800 lb. cattle in Nebraska have stabilized at around $260 per cwt. Looking ahead, the basis—a measure of the difference between cash market prices and futures prices—is expected to remain high. Currently, the basis stands around +30 for 700-800 lb. cattle and +75 for 500-600 lb. steers in Nebraska, reflecting strong cash market conditions. These levels are near all-time highs, suggesting solid market appreciation for feeder cattle prices despite broader volatility. The anticipation of herd rebuilding during the fall and winter could further drive prices higher, potentially continuing into 2025.

Live Cattle Market Mirrors Feeder Market Uncertainty

The live cattle market reflects similar uncertainties. The December contract dropped by $5 per cwt. over the past week, with resistance remaining around $173. There is a possibility that the market could move another $1.50 lower to reach a resistance level similar to that of December 2023. To push beyond this level, however, a significant market driver would be required.

Several factors could impact live cattle prices in the coming months, including feed costs and carcass weights. Feed costs are decreasing due to a historically large corn crop and low-priced distillers' grains, which reduces the cost of feeding cattle for longer periods. However, there is ongoing debate over whether producers will aim for heavier weights on existing cattle rather than placing relatively more expensive feeder cattle. Harvest weights are unusually high but are beginning to align with seasonal patterns. If current trends continue, steer weights could reach 960 pounds by the fall, creating challenges for feedlots, some of which have already faced heavy cattle discounts. It remains to be seen whether processing plants will be able to manage a lower cattle supply with heavier weights profitably. The narrowing Choice-Select spread, which reflects an increased preference for leaner beef, is likely to play a role in these decisions.

Shifting Beef Cutout Dynamics

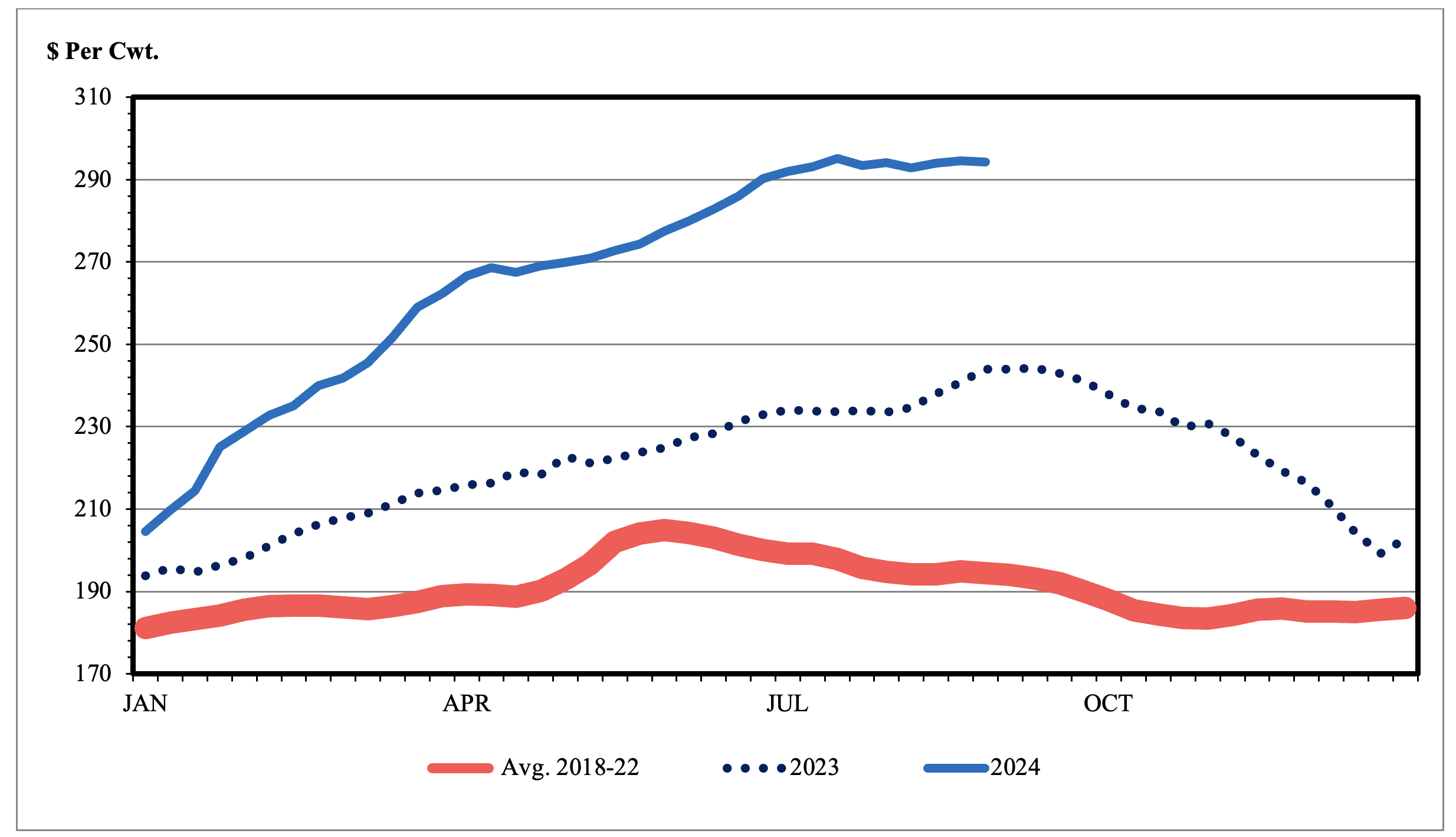

One driver of the narrowing Choice-Select spread is the strong market for ground beef, which is made from beef trimmings. Beef trimmings from fed cattle are typically 50% lean, while those from cull cows are 90% lean. These two products are often mixed in a five-to-one ratio to produce an 80/20 lean-to-fat blend. Currently, there is a shortage of lean beef products in the market, which incentivizes producers to focus on producing more select carcasses. This trend is partly driven by the high cutout value for cull cows, which is around $290 per hundredweight (cwt). For comparison, the cutout value for Choice steers is $310 per cwt, meaning that all products from a cull cow carcass are almost as valuable as those from a fed steer.

These high prices are encouraging significant pull-through of cattle for slaughter. Earlier in the year, most of the slaughtered cows came from beef herds, but in recent weeks, there has been a shift toward dairy cows. This shift reflects the extremely strong demand for ground beef products, which is currently driving the market. As we move into the fall, it remains to be seen whether this demand will continue and whether consumers will be willing to pay higher prices for basic products like ground beef.

Figure 1. Boxed Cow-Beef Cutout Value, Cutter Cow, Weekly

Source: USDA-AMS (2024) from LMIC (2024)