USDA/Flickr (Public Domain)

Listen: Nebraska FARMcast

This article was first published by "Nebraska Cattleman" magazine.

Much work has been done on illustrating the benefits and performance of price risk management tools available to livestock producers. These tools include futures and options available through the Chicago Mercantile Exchange (CME), video/cash contracts, basis contracts, and more recently Livestock Risk Protection (LRP) insurance offered through USDA’s Risk Management Agency (USDA-RMA). These conversations are productive and often lead to a greater understanding of what the tool is, how it works, what types of risk it protects against, and more importantly what types of risk it does not protect against. For example, the use of LRP sets a minimum price producers will receive subject to basis risk. Producers pay a premium ($/cwt.) for the total amount of production insured. A producer receives a payout if the actual price is lower than the insured price at the time the contract expires. These conversations about specific tools often help producers understand the tools available and clarifies and gives assurance that the tool works as they believe it should.

In the excitement about learning how to use new/different price risk management tools that fit with our operations goals and objectives, we can sometimes miss a more fundamental question: Which tool should I use to manage price risk given current and future market situations? If this question is not asked, it has the potential to lead to expressing frustration that the tools don't work as well as they should. While in some cases this may be true (e.g., lack of convergence in basis or the Holstein market collapsing and LRP not paying out), most of the time it is the mismatching of price risk management tools to market situations. Here is a practical example we can all relate to. Let’s say we are building a shed and we are trying to fasten two 2x4s together. We do this by taking nails and driving nails into the boards with a hammer. Most of us would laugh if we were working with someone and they instead grabbed a saw instead of a hammer. Why is this? It's because there is a general understanding that hammers and nails fasten boards together, not saws. The same applies to price risk management tools. We need to match the appropriate tool to the appropriate market situation.

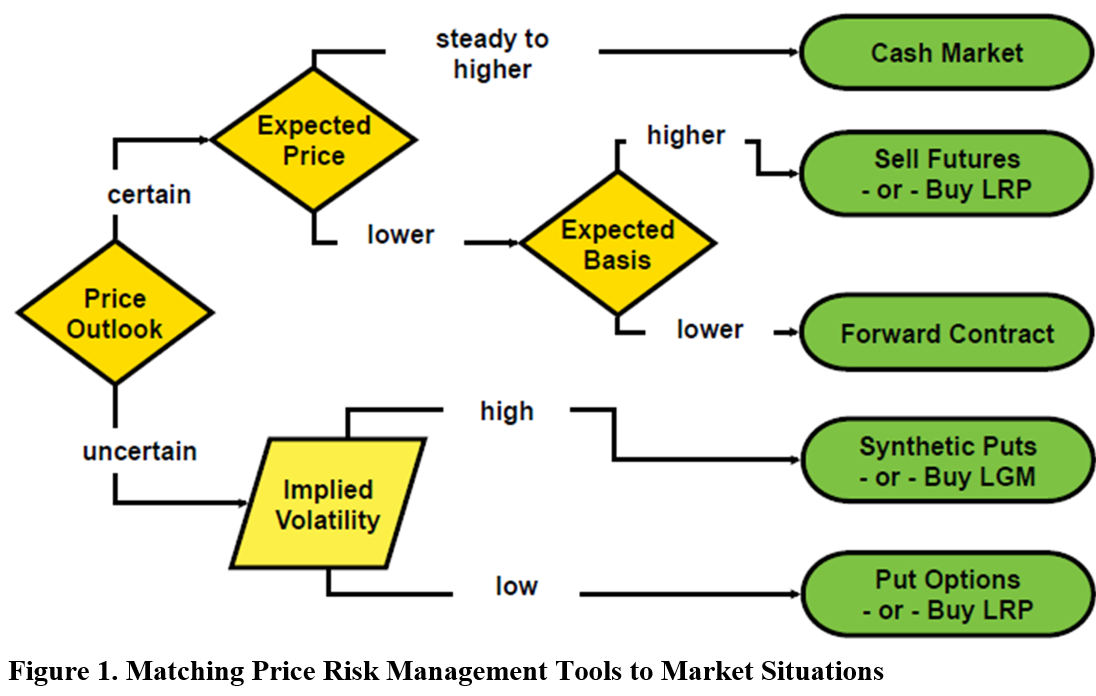

Figure 1 is the most straightforward way of explaining this concept that we have found. While it leaves out several nuances of how these tools work, this figure provides three questions producers can ask an outlook presenter, ag news/media, marketing partner, or other producers at the coffee shop. These questions include:

1) What is your expectation/observation about price: certainty and direction?

2) What is your expectation about the basis (basis = local cash price – futures price)?

3) What is your expectation/observation about price volatility?

These questions can start the conversation and lead to a better application of available tools. One tool that we have talked more frequently about these past few years is LRP which is a tool like an “at-the-money” or an “out-of-the-money” put option that producers can purchase from a USDA-RMA crop insurance agent. Beginning in 2018, USDA-RMA increased the federal subsidy levels on LRP from 13% regardless of the coverage level to anywhere between 35-55% - higher subsidy levels for lower coverage prices. These, and other notable changes, have made LRP a much more attractive and affordable price risk management tool for livestock producers to use. However, should LRP always be used as a price risk management strategy? No! LRP is a great tool with several benefits such as flexible contract sizes rather than fixed contract sizes required by CME and premiums due at the end of the insured period. Still, using LRP during inappropriate market situations can result in poor outcomes. So when should we use LRP? Using the flow chart from Figure 1, LRP would be an appropriate tool if either 1) we are certain price is going lower and basis is going higher (strengthening) or 2) we are uncertain about price and price volatility is low. Similar scenarios could be created using CME futures, CME options, video contracts, or staying in the cash market. Yes, there are market situations where producers should take all the risks in the cash market. But this should be a conscious choice rather than something done out of habit or ease.

Perhaps some of this misapplication of price risk management tools to market situations falls on risk management professionals not clearly explaining how tools and market situations align. This article is one attempt at dispelling some of those price risk management myths. We hope to continue to work on these education and clarification efforts with livestock producers in Nebraska. During the spring, summer, and fall of 2022, the University of Nebraska – Lincoln will hold 8-10 risk management meetings around the state further explaining available tools, how they are to be used, and most importantly when they are to be used. If you or someone you know would have an interest in attending one of these meetings, please reach out to Elliott Dennis, Jay Parsons, or the Department of Agricultural Economics Center for Agriculture Profitability (https://cap.unl.edu/) and we’d be happy to get you connected with a meeting nearest you.

Figure 1. Matching Price Risk Management Tools to Market Situations

This material is based upon work supported by USDA/NIFA under Award Number 2018-70027-28586.

Elliott Dennis is a Livestock Marketing and Risk Management Economist at the University of Nebraska–Lincoln

Jay Parsons is a Farm and Ranch Management Specialist at the University of Nebraska–Lincoln