This article was originally published by "In the Cattle Markets" in August 2022.

Over the last several weeks there have been ongoing, heightened tensions between the U.S. and China over the Taiwan situation. This has caused some concern among producers about the sensitivity of the U.S. beef industry to Chinese purchases. Only several years ago, President Trump signed a trade deal with China in which the Chinese committed to purchasing additional U.S. exports in two phases. This has significantly raised the total quantity and value of beef leaving the U.S. to mainland China and strengthening the U.S. wholesale beef price. Even with the emergence of the COVID-19 pandemic, the Chinese have continued to purchase U.S. beef.

U.S.-China Trade Agreement

The U.S.-China trade agreement did five primary things for the U.S. beef industry. One, it allowed for the continued protocol for the importation of U.S. beef and beef products into China. Two, China eliminated the cattle age requirements for the importation of U.S. beef and beef products. Three, China recognized the U.S. beef and beef products traceability system, acknowledged that there was a negligible risk of bovine disease, and agreed to follow the OIE standards if the U.S. health status would change. Four, it allowed for the importation of beef and beef products into China that was inspected by the USDA’s Food Safety and Inspection Service (FSIS). Five, China adopted maximum residue limits for several hormones. Collectively, these five conditions allowed for more beef to enter mainland China.

Historical Performance of Chinese Imports of U.S. Beef

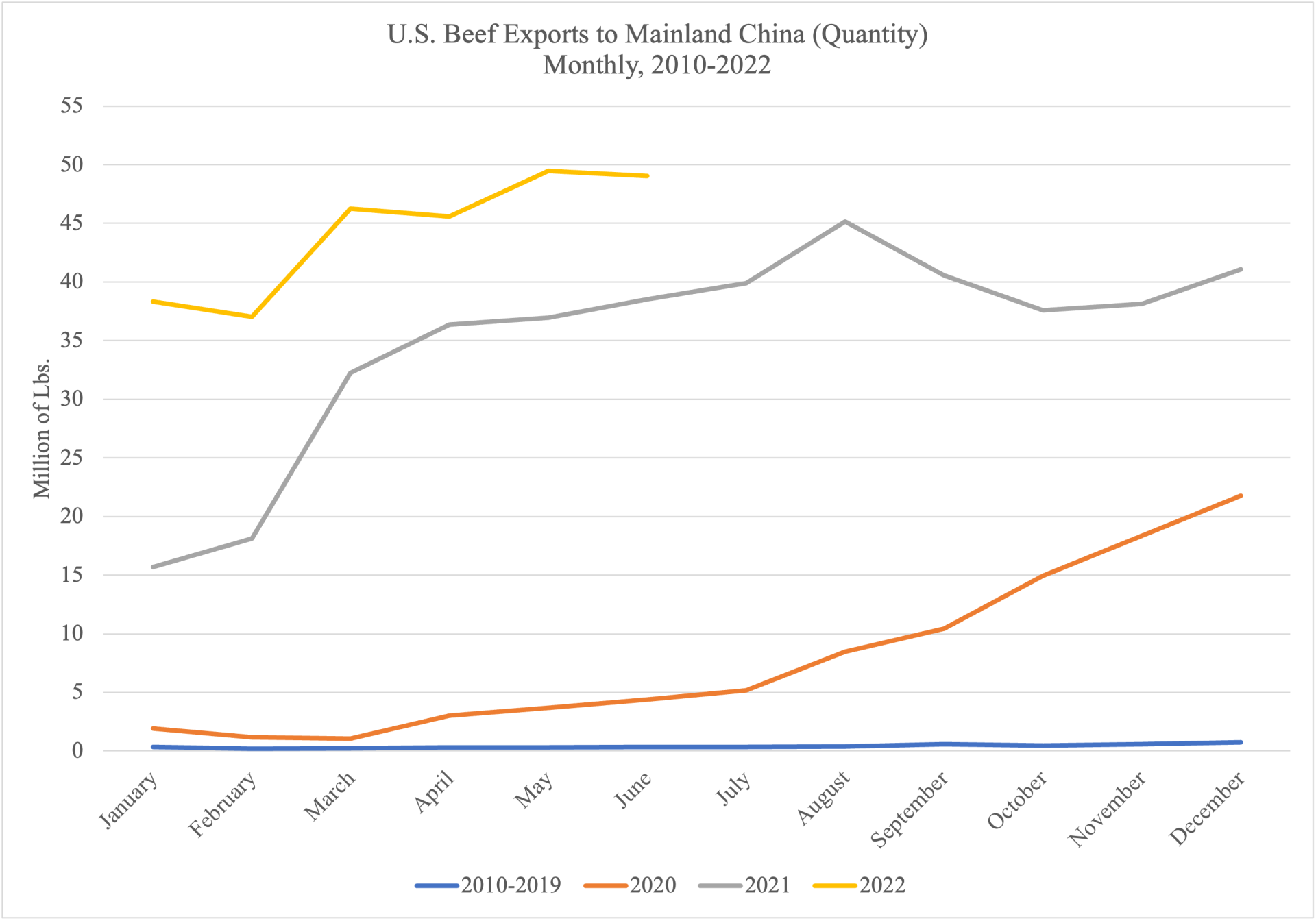

There was a minimal amount of beef that entered directly into mainland China before the two-phase trade deal, with no single month topping one million pounds exported. China is now the third-largest importer of U.S. beef based on total quantity, importing an average of 35 million lbs. of beef per month in 2021. Japan and South Korea continue to remain the U.S.’s largest trading partners with an average monthly export quantity of 58 million and 51 million lbs., respectively. The total quantity shipped to China from the U.S. in 2022 is higher than in 2021 by about 10 million lbs. per month. This brings their current market share to 17% of total U.S. beef exports. Based on data from 2021, we should see seasonal exports to China increase through August and then expect some decrease through the latter part of the year (see Figure 1). Granted, this seasonality could differ given the industry only really has one complete year of purchase information.

Vulnerability of the U.S. Beef Complex to Chinese Policies

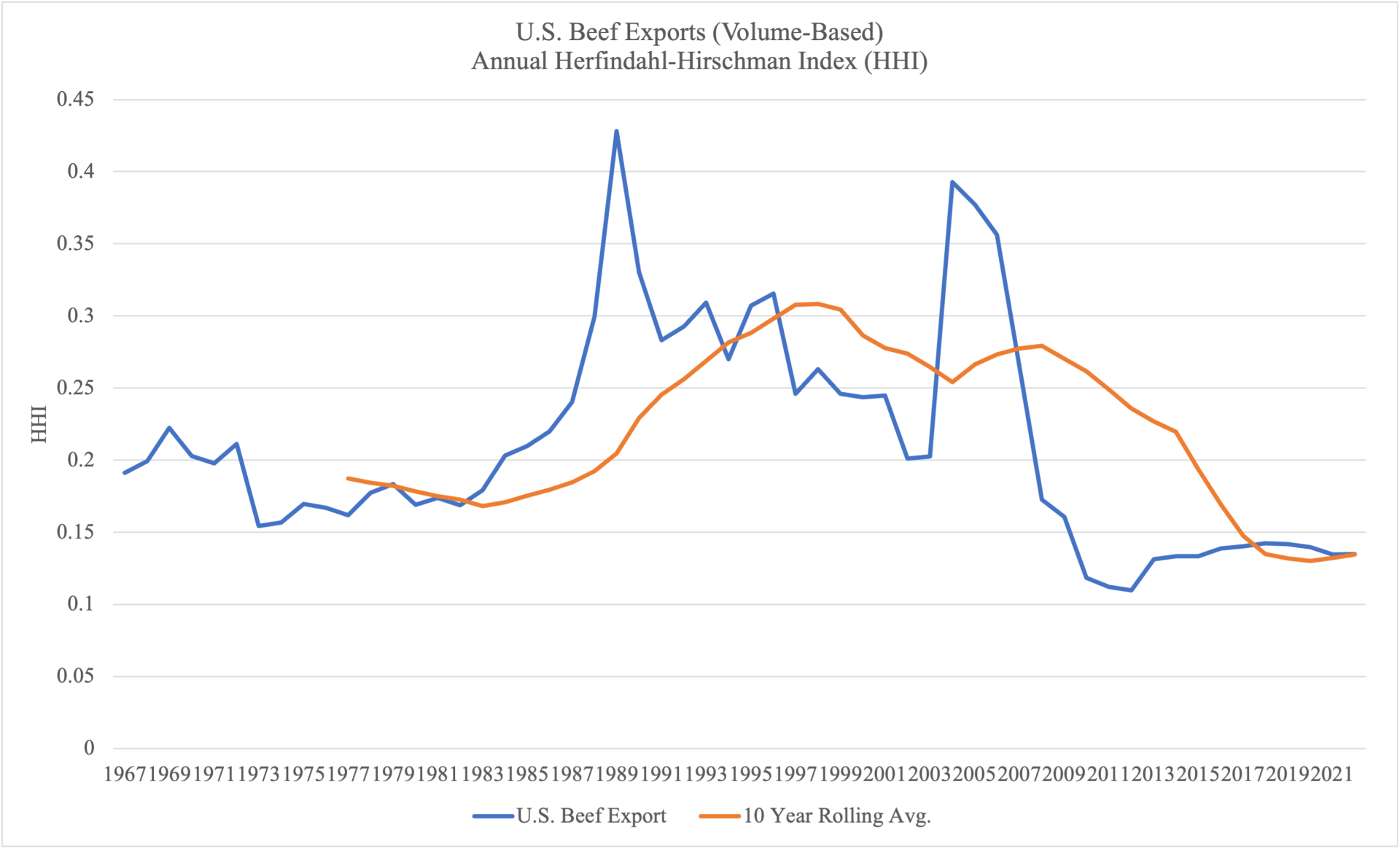

Some industry participants have expressed concern that the Chinese entering the market now makes the U.S. beef complex more vulnerable to the perceived subjective policies in China. One can test for this using a measure of market concentration (see Tonsor (2018) for a detailed example). Between 2010-2019, the average measure of concentration was 0.128 (0 is highly competitive and 1 is highly concentrated). When the Chinese stepped in and started buying U.S. beef beginning in 2020, the measure of concentration changed from 0.152 to 0.146 in 2020 and 2021, respectively. Year to date, the measure of concentration in 2022 is 0.149. The U.S. beef export market has become more concentrated in recent years but is far less concentrated than it was in the 1990s when the measure of concentration was approximately 0.312. In other words, the U.S. beef export market is not as vulnerable as some industry participants currently claim (see Figure 2).

U.S. Beef Export Market Stronger After BSE?

The concerns with China highlight a larger story about how sensitive the U.S. beef export market is to both internal and external shocks. The largest of these shocks was BSE in December 2003. After BSE, many countries significantly reduced the total amount of trade with the U.S. – total trade quantity dropped by approximately 75%. However, this created opportunities for the U.S. to develop other markets. While the average quantity per country reduced from 25 million per year to 6 million per year between 2003 and 2004, the total number of countries with a positive trade quantity increased from 112 to 118.

That number continued to grow over the next 10 years while the primary U.S. beef export markets recovered. Similarly, the U.S. increased quantities into existing countries which have retained post-BSE trade levels even after the U.S. has regained access to other large export locations. Places like Ukraine, Moldova, Poland, and the Leeward-Windward Islands became major export destinations. The U.S. beef export market has shown that it will continue to expand, even if export access is lost to key countries.

Source: USDA-FAS, BICO (HS-10)

Source: Reproduced and updated from Tonsor (March 2018) “Concentration of U.S. Red Meat Exports” available at https://agmanager.info/livestock-meat/marketing-extension-bulletins/trade-and-demand/concentration-us-red-meat-exports